Inside a wind turbine

By Nate Louf

As someone who has done several cross-country road trips, I've come to appreciate the obscure and esoteric attractions as much as the Hoover Dams and Route 66s. One such energy-related attraction is the wind turbine blade display in Weatherford, Oklahoma. The blade shows both the scale of the engineering and the detail of the artwork painted on it.

A modern wind turbine is one of the largest moving machines ever built. Many of the interesting current events in the wind sector (the offshore size race, the rise of Chinese OEMs, the recycling and rare earths problems, political viability) are driven by the physics and material constraints of the machine itself. Understanding the object is useful to understanding the industry.

Three takeaways at the top. First, the size race is the dominant force shaping the industry, with rotor diameters tripling and swept area growing roughly eightfold since the late 1990s. Second, manufacturing leadership has shifted decisively to China, with Chinese OEMs holding the top four positions globally for the first time in 2024. Third, the physical constraints on the next decade of turbine progress are not aerodynamic but logistical and material: recycling, rare earth supply, and, for offshore, port and installation infrastructure.

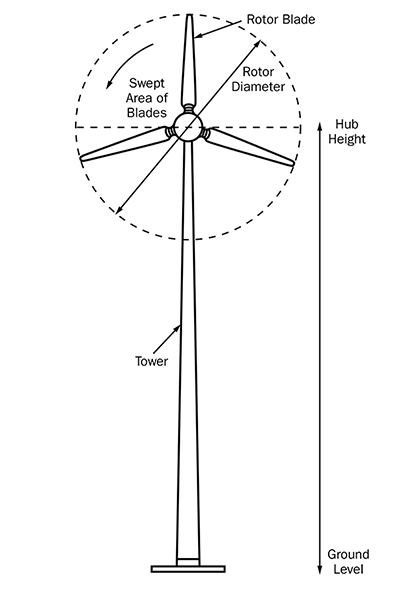

Anatomy

A horizontal-axis wind turbine, which is what a vast majority of utility-scale machines are, has four major sections: the rotor, the nacelle, the tower, and the foundation.

The rotor consists of three blades and the hub that bolts them together. Each blade is an airfoil, like an airplane wing, with a twist of 15 to 25 degrees from root to tip. The reason for the twist is that the tip of the blade travels much faster than the root — on a 115-meter blade, the tip can move at over 80 meters per second while the root is barely moving, so the angle of attack must vary along the length to maintain consistent lift. A pitch bearing at the root of each blade allows the entire blade to rotate, which is the primary control mechanism for output above rated wind speed.

The nacelle is the most concentrated piece of engineering in the machine. It contains the main bearing, the main shaft, either a gearbox stepping the 10–15 rpm rotor speed up to 1,500 rpm for the generator or a direct-drive system that skips the gearbox entirely, the generator itself, the yaw motor that rotates the nacelle to face the wind, the power electronics, and the cooling system. On the back of the nacelle sit two of the most important sensors on the entire machine: an anemometer and a wind vane, both feeding the yaw and pitch control loops.

The tower is almost always tubular steel, occasionally concrete or hybrid and painted off-white. The white paint color is chosen to satisfy aviation authority visibility requirements, reflect solar radiation away from the nacelle and blade composites, and extend the life of the UV-sensitive fiberglass coatings over the turbine's 20–30 year service life. It tapers from base to top and contains a service ladder or small lift. The tower's height is consequential because wind speed increases with elevation: doubling height in open terrain can add roughly 10% to wind speed and 33% to available power, owing to the cubic relationship between wind speed and power output.

The foundation is where onshore and offshore turbines diverge. Onshore turbines sit on a concrete spread footing (typically 600 to 1,000 cubic meters of concrete and around 110 tons of rebar, buried just below grade). Offshore options include the monopile (a single steel tube up to 12 meters in diameter, hammered into the seabed, used in over 80% of installed offshore turbines), the jacket (a four-legged steel lattice for deeper water, similar to oil platform substructures), and floating platforms for water deeper than roughly 60 meters. Floating wind currently represents only about 250 MW of operating capacity globally but is the only economically viable approach for the majority of the world's deep-water offshore wind resource.

The size race

Utility-scale wind turbines have roughly tripled in rotor diameter over the last 25 years.

Average new U.S. onshore turbine capacity has grown roughly fivefold since the late 1990s. Average rotor diameter has tripled. Average hub height has nearly doubled. The combination of taller turbines and longer blades has resulted in swept area, which determines how much wind energy the turbine can extract, growing by approximately a factor of eight.

Offshore is where the size race is currently most aggressive. The largest commercial and prototype turbines as of early 2026 are all in the 14–26 MW range, with rotor diameters from 220 to 310 meters.

Two observations stand out. First, Chinese OEMs are leading at the frontier. Mingyang installed a 20 MW prototype in Hainan in August 2024, Dongfang announced a 26 MW machine in October 2024, and CRRC is building a 20 MW floating prototype. Second, the size race is bifurcating. Western OEMs (Vestas, Siemens Gamesa, GE Vernova) have effectively settled in the 14–15 MW range as their commercial frontier, while Chinese OEMs continue to push to 18, 20, and 26 MW.

The economic logic for size growth is straightforward. Swept area scales with the square of rotor diameter, so doubling the rotor quadruples the area available to extract energy. A larger rotor relative to a fixed-size generator (the industry term is "low specific power") means the turbine reaches its rated output more often and produces a higher capacity factor, even at marginal sites. This is why fleet-wide U.S. capacity factors have risen from the mid-20s in the early 2000s to roughly 35% today, with the best new offshore projects in the North Sea operating above 50%.

Innovators argue for continued size expansion to improve capacity factors and reduce levelized cost. Developers increasingly argue for manufacturing volume on mature designs over frontier expansion; the Siemens Gamesa 4.X and 5.X quality crisis, which has cost the company over €1.5 billion in repairs, is the main evidence cited for that view.

Why three blades?

The three-blade configuration is universal across utility-scale turbines. The industry converged on it independently across multiple geographies in the late 20th century, establishing it as the clear engineering optimum.

Two-blade rotors are aerodynamically more efficient than three-blade rotors by roughly 2 to 3% per unit of swept area, while four-blade (and greater) rotors introduce additional capex and opex for minimal additional performance gain.

Mechanical loads. A two-blade rotor has different inertia depending on whether the blades are oriented vertically or horizontally at any given moment. As the rotor turns, this asymmetry creates a wobbling load that has to be absorbed somewhere, typically through a teetering hub that adds complexity, weight, and a known wear point. A three-blade rotor distributes mass evenly through every rotation, presenting roughly constant inertia regardless of orientation.

Diminishing returns. Going from three blades to four buys 1 to 2% more energy capture but adds approximately 33% more blade material and weight, plus another failure point. Going from three to two saves a blade but introduces the wobble problem above. Three is the local optimum, and it has held for forty years.

A modern wind turbine with a number of blades other than three is almost certainly a research prototype or pre-1990 design.

Manufacturing landscape

The most consequential development in the wind manufacturing market over the last several years is the shift in OEM leadership to China.

For the first time in industry history, the top four turbine manufacturers globally by 2024 installations are all Chinese: Goldwind, Envision, Windey, and Mingyang. Vestas, the long-standing Western leader, ranks fifth. Six of the top ten OEMs are Chinese.

Two important caveats temper this picture. First, the Chinese manufacturing base is heavily concentrated to Chinese installations. Roughly 91% of Goldwind's 2024 installations were domestic, and the same pattern broadly holds across the other Chinese names. Second, Western OEMs continue to dominate markets outside China: Vestas, Siemens Gamesa, GE Vernova, and Nordex collectively hold approximately 92% of the European market and 96% of the U.S. market.

The signal worth tracking is whether Chinese OEMs successfully expand abroad. The 2024 export figures are notable: Chinese OEMs won approximately 26.1 GW of orders outside China, up 70% year-over-year. Mingyang in particular has pursued aggressive European expansion: an 18.8 MW supply contract for Italy's 2.8 GW Med Wind floating project, a partnership with Octopus Energy on up to 6 GW of UK onshore, and a £1.5 billion integrated factory announcement in Scotland with first production targeted for 2028.

These plans face active political resistance. Germany's Luxcara was forced to swap Mingyang for Siemens Gamesa on its 300 MW Waterkant project under government pressure. The Trump administration has formally warned the United Kingdom against Chinese turbine procurement on national security grounds. Whether the Chinese OEM export push survives this resistance is the central manufacturing question for the next several years.

The Western manufacturers are in different conditions. Vestas posted 2024 revenue of €17.3 billion and a record €68.4 billion order backlog, suggesting the company has weathered the inflation and supply chain shocks of 2022–23. Siemens Gamesa is still working through its 4.X and 5.X onshore platform quality crisis, with cumulative repair charges exceeding €1.6 billion. GE Vernova spun out of GE in April 2024, absorbed a $379 million loss on its Haliade-X program in 2023, and has effectively retreated from the offshore frontier to focus on a 15.5 MW "workhorse" model.

Materials and constraints

A typical onshore 3 MW machine is approximately 66–79% steel, 5–17% cast iron, 11–16% composites, and roughly 1% copper. The tower alone accounts for approximately 80% of the steel content. Three material-related issues warrant attention.

Blade composites and recycling. Modern blades are roughly 70% fiberglass-reinforced epoxy with a balsa or PVC foam core, increasingly with carbon fiber in the load-bearing spar caps. Thermoset epoxy does not melt, which makes blades fundamentally difficult to recycle. The historical disposal options of landfill or shredding for cement-kiln fuel are decreasingly pursuable options. Germany, the Netherlands, Austria, and Finland have already banned composite landfilling. Vestas has commercialized a chemical recycling process called CETEC and Siemens Gamesa has a deconstructible "RecyclableBlade" product but both are early-stage. With a large cohort of early-2000s blades approaching end-of-life, blade recycling is migrating from a technical curiosity to a binding industry-wide constraint.

Permanent magnets and rare earths. Direct-drive turbines use neodymium-iron-boron magnets, requiring approximately 500 kg of magnet material per megawatt of capacity. In response to United States tariffs, China imposed export licensing on heavy rare earths and finished magnets in April 2025, creating a supply chain constraint. The industry response is engineering substitution but most of the alternatives are not yet proven at scale.

Operational sensitivity to alignment. A turbine misaligned with the wind by 10 degrees loses approximately 4–5% of its output; at 20 degrees, the loss is roughly 16%. The wind vane on the back of the nacelle is among the highest-leverage sensors on the entire machine, despite costing only a few hundred dollars.

What this implies

First, the binding physical constraints on the next decade are largely logistical rather than aerodynamic. The basic turbine architecture is mature. Setting aside politics and economics (which are far and away the main drivers of deployment), the logistical questions that will influence turbine engineering are: can blade recycling scale fast enough to meet end-of-life volumes and emerging landfill bans, can rare earth supply chains diversify away from Chinese export controls and for offshore, can port infrastructure and installation vessel capacity keep up with the size race.

Second, offshore wind is where the live economic, technical, and political questions are. Floating wind is the only path to most of the world's deep-water offshore resource, but only about 250 MW is currently operating. The Chinese OEMs are leading at the size frontier but face increasing political resistance abroad. Western OEMs are retrenching and consolidating. The next two to three years of order books and project sanctioning will determine whether offshore wind grows or stalls.

Third, onshore and offshore wind have diverged enough to be analyzed as separate industries. Onshore is mature, cost-competitive, and under less political scrutiny; offshore is capital-intensive, supply-chain-constrained, and politically contested.

Scale, supply chain, and politics will shape the next decade of wind more than engineering will.

Sources

- Lawrence Berkeley National Laboratory. Land-Based Wind Market Report: 2024 Edition. Primary source for U.S. onshore turbine size averages, fleet capacity factors, and project economics.

- National Renewable Energy Laboratory. Cost of Wind Energy Review: 2024 Edition. Source for cost composition, foundation types, and reference turbine specifications.

- Global Wind Energy Council. Global Wind Report 2025 and Supply Side Data 2024. Cumulative installed capacity and OEM market share.

- Vestas. V236-15.0 MW product specifications and Annual Report 2024. Source for hero turbine specs and 2024 financial figures.

- BloombergNEF. "Chinese Manufacturers Lead Global Wind Turbine Installations." March 2025. Top 10 OEM ranking by 2024 grid-connected capacity.

- Wood Mackenzie. "Chinese OEMs sweep the global wind podium for the first time." March 2025. Confirmation of Chinese top-four sweep and regional market share splits.

- U.S. Geological Survey. What materials are used to make wind turbines? Source for material composition by mass.

- International Renewable Energy Agency. Critical Materials for the Energy Transition: Rare Earth Elements. 2022. Source for permanent magnet content per MW.

- OffshoreWind.biz, Windpower Monthly, JEC Composites, and Blackridge Research. Industry tracking for largest commercial and prototype turbines including Mingyang MySE 18.X-20MW, Dongfang H260-26MW, Goldwind GWH252-16MW, SANY SI-270150, and CRRC floating prototype.

- Energy Connects, Dialogue Earth, reNews, OffshoreWind.biz, and Windpower Monthly. Coverage of Mingyang Scotland factory announcement and Luxcara/Waterkant project swap.

This note is for informational purposes only. OEM market share figures are composites of BloombergNEF, Wood Mackenzie, and GWEC reporting; methodologies vary slightly between sources (grid-connected vs. mechanically installed) and exact rankings may differ at the margins.